This analogy just reminds us, there is never a bad time if you have a long time horizon.

I love orchards and fruiting plants. So, I have a habit of visiting plant nurseries and gardening stores just to gather information, even when I’m not sure what I’ll buy. One day I went to a garden centre to look at apple trees. I asked the owner, “So when is the best time of year to plant an apple tree?” He responded, “Now.”

Unfortunately, I still needed to do quite a lot of work to prepare the ground and I wasn’t quite ready to purchase an apple tree at that moment. But I made a note to myself to come back at the same time next year. About 6 months later, I found myself back at that same garden centre gathering more information. Again, I was looking at apple trees and once again asked, “When is the best time of year to plant an apple tree?” The owner responded, “Now.”

“Wait a minute,” I retorted, “didn’t you say that six months ago was the best time to plant an apple tree?” The owner looked at me wisely and said, “The best time to plant an apple tree was actually 10 years ago.”

A lot of investors ask themselves the question, “When is the best time to invest in shares?”

They may think, “prices are down, now is a good time to invest.” Or perhaps they think, “prices are down, maybe I should wait.” But by trying to figure out the right time to invest in shares, most investors really just accomplish one thing. They don’t invest in shares.

Most investors we work with count their investing time horizon in decades. With advances in modern medicine, a 65-year-old new retiree should really think about their money lasting three decades. If that’s true of a 65-year-old, then a 40 or 50-year-old may have half a century to invest. The reality is that for an investor that counts their time horizon in decades rather than months, there is never really a bad time to invest in shares.

But how can that be true?

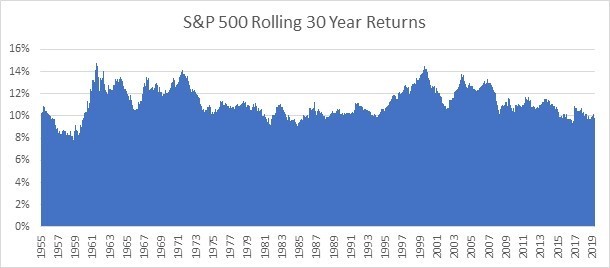

Well, just look at the long-term data. It’s possible to look at 30-year investment windows to see how shares have performed. We can view data for the S&P 500 Index going back to January 1926. For example, if you invested in January 1926, you would have completed 30-years of investment by December 1955. This 30-year window would have included the Great Depression, World War II and the Korean War. Given these events, you’d think this time frame wouldn’t be a particularly good time to invest. However, over that 30-year window, the S&P 500 Index earned a compound return of 10.2% per annum. From December 1955 until March 2020, we can examine a further 772 different rolling 30-year windows to see how all long term investors in the S&P 500 Index would have fared. What is startling in the chart below is the consistency of returns which, two thirds of the time, range between 9% and 12%.

S&P 500 Index returns are in USD

During the best performing 30-year window, an investor earned a compound return of 14.8% per annum. But even over the lowest performing 30-year window, an investor still earned a tidy 7.8% per annum compound return. The investors who achieved the 7.8% p.a. returns started investing the month before the 1929 share market crash. Still, if they stayed the course and maintained their investment, their returns would have been just fine. The median return over all rolling 30-year periods was 10.9% p.a.

In New Zealand, we can look at NZX50 gross index returns going back to July 1991. For those counting, that is 345 months ago. So, it will be a little over a year until we complete our first 30-year time horizon using that particular index. However, we can still calculate the returns if an investor had started investing in July 1991, and simply bought and held the NZX50 index.

Our last complete month of observations was March 2020 when the NZX50 index experienced a negative 13% return. All the same, an investor who began investing in the index July 1991 and maintained their investment, experienced a compound return of 9.54% p.a. Remember, this time period includes the Asian Financial Crisis, the tech wreck, the Global Financial Crisis and the start of the COVID-19 downturn. It includes all those shaky markets, yet the compound return is still 9.54% p.a.

With this in mind, I can see the wisdom of the person selling fruit trees. In my back yard I have a pear tree which is approximately 30 years old. This season it produced a bumper crop of fruit, so much that I gave fruit away, bottled what I could, ate fruit every day along with my entire family and I still couldn’t keep up. But those apple trees I bought just a few years ago… well let’s just say that they are coming along.

If I want a productive garden of fruit trees the most important thing is to start. The timing isn’t the critical element. The man at the store knows that when people feel it isn’t the perfect time to plant a tree they delay, they move on to other things, they forget about it, and often they’ll miss years of productive growing time, all because they were waiting for the perfect time.

For most of us investing for a lifetime, the time to start is nearly always now or even better, 10 years ago. As the phrase goes, it’s time in the market rather than timing

the market that really matters, for the investor and for the amateur orchardist.